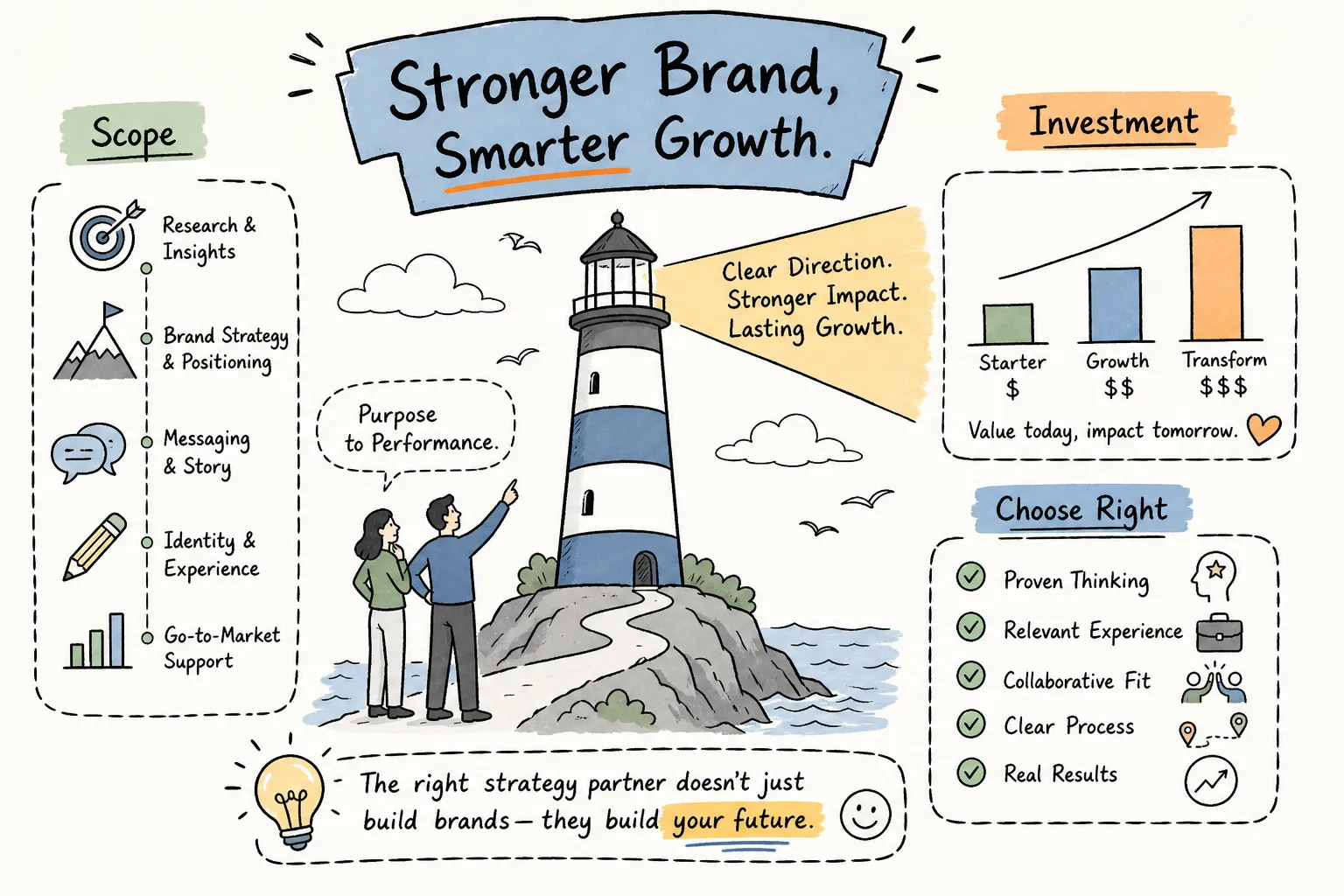

How to Choose a Bank Marketing Firm That Actually Moves the Needle

Most banks look and sound exactly the same online. The same stock photos of smiling families, the same vague promises about “trusted relationships,” and the same forgettable content that does nothing to drive new accounts or deepen customer loyalty. If your institution is stuck in this cycle, the problem likely is not your product. It is your marketing partner.

Choosing the right bank marketing firm is one of the most consequential decisions a financial institution can make, yet many banks rush through the selection process or default to whoever offers the lowest retainer. The result is wasted budget, missed growth targets, and a brand that fails to stand out in an increasingly competitive landscape.

This guide is built for banking professionals who already understand the basics of marketing and are ready to make a smarter, more strategic choice. You will learn the specific criteria that separate average agencies from those that deliver measurable results, the red flags to watch for during the vetting process, and the key questions that reveal whether a firm truly understands the financial services industry.

Why Choosing the Wrong Bank Marketing Firm Is a Strategic Risk

The stakes of selecting the right bank marketing firm have never been higher. According to the ABA Banking Journal’s 2026 channel investment survey, 83% of bank marketers plan to increase digital advertising budgets in 2026, meaning every dollar allocated to a misaligned agency partnership carries greater consequence than ever before. When budgets scale upward, strategic errors do not simply cost money; they accelerate in impact.

Digital media is projected to comprise 65 to 70% of bank marketing budgets by 2026, a concentration that makes execution quality and strategic alignment genuinely non-negotiable. At that level of digital dependency, an agency that cannot maintain coherent brand storytelling across paid search, social, display, and content channels does not just underperform; it actively fragments the customer experience at the moments that matter most.

The competitive context intensifies the risk further. Fintech competitors and neobanks are capturing checking accounts by outspending community and regional banks on brand experience, with fintech bank holding companies allocating roughly 8.45% of noninterest expense to marketing compared to under 2.6% for traditional banks. Winning on differentiation, not volume, is the only viable response.

Compounding this pressure, AI-generated content is flooding the financial services space. As marketing budget and staffing data for 2026 confirms, authentic brand conviction is becoming the scarcest and most valuable currency in banking. A wrong agency partner does not just waste budget; it erodes brand coherence across every digital, physical, and experiential touchpoint a customer encounters, quietly dismantling the trust that took years to build.

Criterion 1: Real Financial Services Expertise, Not a Banking Practice Bolt-On

The distinction between an agency that has built genuine financial services expertise over years of practice and one that has simply added a “banking vertical” to its capabilities deck is not cosmetic. It is structural. Generalist agencies entering banking as a revenue diversification play tend to approach the sector with frameworks borrowed from consumer goods or technology, categories where regulatory guardrails are minimal and brand messaging carries far lower stakes. In banking, every claim is subject to scrutiny. Compliance with regulations governing advertising disclosures, deposit account promotions, and lending communications is non-negotiable, and agencies without deep sector experience routinely produce work that either underperforms or creates institutional risk.

When evaluating a bank marketing firm, the breadth of its institutional experience matters as much as the depth. A firm that has only served community banks will struggle with the complexity of a regional institution managing multiple lines of business. Conversely, an agency with experience across community banks, regional banks, credit unions, and fintechs demonstrates genuine adaptability. Each institution type carries distinct strategic demands: credit unions operate on member-ownership dynamics that shape messaging entirely differently than shareholder-driven banks; fintechs require digital-native acquisition models that traditional banking agencies rarely understand from the inside out.

Client rosters deserve direct scrutiny during the evaluation process. Ask prospective partners to share work with institutions comparable in asset size, product complexity, and competitive context to your own. According to research on selecting financial services marketing partners, agencies with relevant portfolios reduce onboarding risk significantly, because they arrive with proven approaches rather than learning on your organization’s budget.

True sector fluency also means the agency understands the economics underlying your marketing objectives. Deposit growth pressure, loan acquisition cost structures, lifetime value modeling, and the direct relationship between brand trust and share of wallet are not concepts that need explaining to a seasoned financial services partner. They are the vocabulary of the engagement from day one. Finance and insurance marketing demands a different standard because every campaign decision carries both regulatory weight and revenue consequences that generalists routinely underestimate.

Finally, look at relationship tenure. Agencies that maintain multiyear engagements with financial services clients signal something important: they deliver consistently enough that institutions trust them through regulatory shifts, competitive disruptions, and leadership changes. That kind of sustained partnership is only possible when an agency has earned its expertise through accumulated institutional knowledge, not a recently launched practice group.

Criterion 2: Brand Strategy Before Execution, Not After

The majority of bank marketing firms operate on a tactics-first model. They open an engagement with a brief discovery call, produce a rudimentary brand platform in the first week or two, and then pivot immediately to SEO audits, paid media campaigns, and email sequences. The brand strategy document becomes a formality rather than a foundation, something to satisfy a project milestone rather than a genuine north star for every decision that follows. With 2026 bank marketing budgets increasingly weighted toward digital channels, the pressure to show fast, measurable results intensifies this tendency, pushing strategic depth further down the priority list.

The problem is not the tactics themselves. SEO, paid media, and email are legitimate and necessary channels. The problem is sequencing. When a bank marketing firm begins by excavating the belief system at the core of your institution, understanding what your organization stands for and refuses to compromise on, the resulting marketing compounds. Every campaign reinforces the same positioning, every channel sends consistent signals, and your institution builds cumulative equity in the market. When strategy is absent or perfunctory, campaigns produce diminishing returns and require perpetual reinvestment to sustain even modest visibility.

Brand strategy delivers something tactically irreplaceable: a positioning framework, a messaging architecture, and a narrative structure that make every downstream execution more efficient and more coherent. Your SEO content targets the right audiences with language that resonates rather than generic financial keywords. Your paid media speaks to a defined prospect with a clear value proposition. Your email sequences feel like a natural extension of a relationship rather than isolated promotional pushes. Financial institutions marketing strategies that lack this foundation consistently struggle with channel fragmentation, where the website says one thing, social media says another, and branch-level communications say something else entirely. Prospects receive inconsistent signals and trust erodes before a relationship ever begins.

The diagnostic question to ask every prospective firm is straightforward: walk me through exactly how many discovery, research, and strategy engagements precede any creative execution or campaign launch. A firm with genuine strategic conviction will describe a phased process spanning weeks, encompassing competitive analysis, audience research, positioning workshops, and messaging validation before a single ad is written or a single keyword is targeted. A tactics-first firm will describe a compressed brand sprint and an eager pivot to deliverables. The answer reveals the firm’s actual operating philosophy more clearly than any credentials deck or case study reel ever will.

Criterion 3: Regulatory and Compliance Fluency as a Baseline Capability

Regulatory compliance is not a specialty service that deserves a line item on an agency’s invoice. It is table stakes. Any bank marketing firm operating in the financial services space must treat FDIC, FINRA, and CFPB standards as foundational knowledge, not as expertise borrowed from a client’s legal department when a campaign is already in flight.

The exposure is real and broad. Every campaign asset, from a website landing page promoting a deposit product to a social post advertising loan rates, carries regulatory risk. The CFPB’s UDAAP prohibitions against unfair, deceptive, or abusive practices extend across channels and formats. In 2023 alone, the CFPB filed 29 enforcement actions resulting in approximately $3.07 billion in consumer redress and $498 million in civil penalties. According to Luthor.ai’s bank marketing compliance guide, consumer complaints to the CFPB surged 62% year-over-year by September 2023, and misleading marketing claims are among the leading triggers. An agency that produces non-compliant copy does not just create poor creative; it creates liability.

When evaluating a bank marketing firm, ask direct questions about compliance workflows. Does the agency integrate compliance review at the planning stage or only at final approval? Do they maintain in-house expertise, or do they rely entirely on your legal team to catch problems? As Sedric.ai’s 2026 marketing compliance guide notes, best-practice programs embed structured pre-approval processes, disclosure checklists, and post-publication monitoring as standard operations, not reactive measures.

Regulatory fluency also makes agencies better creative partners, not more restricted ones. When an agency understands precisely what it cannot say, it develops sharper instincts for communicating what is genuinely distinctive. Prohibited claims and mandatory disclosures force a discipline that elevates clarity and specificity. According to Sondhelm Partners, experienced financial marketers treat compliance as a framework for stronger communication rather than a barrier to it.

Finally, institutional depth matters. Agencies that have built dedicated financial services practices over years carry accumulated knowledge of product-specific rules, evolving regulatory guidance, and multi-channel disclosure requirements that agencies newer to the sector simply cannot replicate on a compressed timeline.

Criterion 4: Integrated Capabilities Across the Full Brand Lifecycle

Fragmented agency relationships introduce a structural problem that no amount of tactical execution can solve. When one firm owns brand strategy, another manages digital channels, and a third handles social content, the result is narrative dissonance at precisely the touchpoints customers scrutinize most: the website, the onboarding flow, the social feed, the branch experience. Each agency optimizes for its own deliverable rather than the coherent whole, and customers encounter a brand that feels inconsistent, even untrustworthy, across the moments that determine whether they stay or leave.

A bank marketing firm with integrated capabilities across strategy, identity, messaging, digital, content, and experiential design can hold a single thread of brand conviction from the first awareness impression through acquisition, onboarding, and long-term retention. Brand strategy informs identity systems. Identity systems govern digital platforms. Digital platforms shape the personalized content that drives cross-sell and loyalty. When these disciplines live under one accountable team rather than across three separate vendor relationships, coherence is built into the process rather than negotiated after the fact.

This coherence has measurable commercial stakes. Sixty-six percent of consumers are willing to share personal data in exchange for more personalized financial experiences, but personalization only generates loyalty when the brand delivering it feels credible and consistent. Integrated marketing approaches create the trust infrastructure that makes data-driven personalization feel relevant rather than intrusive, a distinction that matters acutely in a regulated, trust-sensitive category like banking.

When evaluating a prospective partner, look beyond single-campaign case studies. Assess whether the agency can demonstrate continuity across a client’s full brand presence: strategy leading into identity, identity carried through digital platforms, platforms supported by content ecosystems, and the whole reinforced through experiential or retention programming. Ongoing client relationships with multi-touchpoint evidence are a stronger proof point than award-winning one-off executions.

Integrated firms also address a practical constraint that most bank marketing leaders know well. Bank marketing departments are often lean relative to the scope of their mandates, managing omnichannel programs with limited internal headcount. Coordinating multiple specialized agencies multiplies management overhead through redundant briefings, misaligned handoffs, and competing priorities. A single integrated partner consolidates accountability, reduces coordination friction, and frees internal teams to focus on strategy and measurement rather than vendor management.

Criterion 5: Proven Results With Financial Services Clients You Can Verify

Any bank marketing firm worth serious consideration should be able to do more than describe its process. It should be able to prove its impact with numbers tied to outcomes that matter to financial institutions: deposit growth, loan acquisition lift, digital onboarding completion rates, and share-of-wallet expansion. Before signing an engagement, require case studies that connect brand and marketing investments directly to these business outcomes. Generic traffic growth or social engagement figures are not sufficient evidence for a strategic buyer. Bank executives need to see that an agency understands how marketing translates into net new accounts, increased balances, and measurable revenue contribution.

The specificity of those metrics matters enormously. Performance data from bank marketing engagements should be calibrated to institution type. A community bank evaluating an agency should expect to see per-branch account growth figures, local deposit acquisition rates, and cost-per-acquisition benchmarks relevant to its market footprint. A regional institution should expect conversion rate data tied to digital onboarding funnels and organic search performance connected to intent-driven queries. The standard shifts depending on scale, but the requirement for precision never does.

Beyond case studies, ask for evidence of asset growth attribution, sustained conversion rate improvements, and organic search performance that can be traced back to brand and content investments over time. These metrics reveal whether an agency functions as a genuine growth engine or simply a production vendor.

Reference clients are equally important. A credible bank marketing firm should readily facilitate introductions to financial services clients who can speak candidly about the engagement experience, the rigor of the process, and the measurability of results delivered. Agencies trusted by recognized financial institutions, those with reputations to protect and regulators to satisfy, have already demonstrated the discipline and strategic depth that executive-level buyers should demand from any partner they bring inside the organization.

Criterion 6: A Global Perspective That Sharpens Local and Regional Positioning

Community and regional banks derive their competitive advantage from proximity, relationships, and local trust. But the brand frameworks that make that trust tangible, defensible, and scalable across every customer touchpoint are shaped by a much broader understanding: how brand conviction travels across markets, cultures, and competitive contexts. Local trust is an asset, but without a sophisticated framework to articulate and protect it, that trust remains fragile and difficult to differentiate from the bank down the street.

Agencies with meaningful international experience bring a benchmarking lens that purely domestic firms simply cannot replicate. They have observed what brand positioning strategies resonate across diverse audiences and geographies, and they carry that comparative intelligence into every regional brief. A firm that has built brands across six continents understands what separates durable conviction from executional noise, and applies that understanding to even the most locally focused engagement.

This global perspective matters more urgently today because regional banks are increasingly competing for customers who have experienced sophisticated international digital banking brands and arrive with elevated expectations around personalization, seamlessness, and omnichannel consistency. Meeting those expectations while preserving authentic local character requires creative ambition informed by global standards, not constrained by domestic conventions alone.

A firm with offices and client portfolios spanning multiple continents also signals something important: organizational maturity. That maturity correlates directly with the process rigor, compliance discipline, and senior talent allocation that complex banking engagements demand. Multi-stakeholder strategy, data governance, and measurable attribution are not improvised in mature international agencies. They are embedded in how the work gets done from day one.

Criterion 7: A Philosophy That Survives AI Saturation and Commoditized Messaging

Generative AI has fundamentally changed the volume and velocity of financial services content. In 2026, banks and their agency partners can produce social posts, email sequences, landing pages, and video scripts at a scale that was unimaginable three years ago. The problem is that every competitor has access to the same tools, the same prompts, and the same optimization playbooks. The result is a saturation of content that looks similar, sounds similar, and ultimately earns similar levels of consumer indifference. Online mentions of “AI slop” surged 200% in 2025, reflecting a growing audience backlash against synthetic, generic output that lacks substance or soul. In banking, where trust is the foundational currency, this commoditization is not a minor inconvenience; it is a direct threat to brand equity.

The agencies best positioned to help banks cut through this noise are not the ones producing the most content. They are the ones operating from a clearly defined philosophy of brand conviction. Volume without conviction produces interchangeable output. When every institution is generating polished blog posts, optimized headlines, and AI-assisted ad copy, the only meaningful differentiator is the belief system that shapes what gets said, what gets refused, and why. Only 41% of marketers can currently demonstrate measurable ROI from AI-generated content, a statistic that underscores how throughput alone fails to move the needle.

Brand conviction is the articulation of what an institution stands for and will not compromise on, regardless of trend cycles, competitive pressure, or platform shifts. It functions as an operating system across strategy, culture, product, and customer experience, ensuring that every touchpoint reinforces a coherent identity rather than a collection of disconnected campaigns. When evaluating a bank marketing firm, demand that the agency articulate its own brand philosophy with the same clarity it would bring to a client brief. If a firm cannot describe what it believes and how those beliefs have shaped lasting, distinctive work in financial services, it is unlikely to build that conviction on your behalf.

Starfish calls this the Brand Creed: a foundational belief system that acts as a decision filter across every dimension of brand expression and organizational behavior. Rather than treating brand as a marketing output, Starfish treats it as the mechanism that aligns strategy, culture, and customer experience into a single, coherent whole. This philosophy ensures that marketing investments compound over time rather than dissipate into the broader saturation, building the kind of durable trust that no AI content pipeline can replicate.

The Questions to Ask Before Signing With a Bank Marketing Firm

The criteria outlined above sharpen your evaluation framework. These five questions translate that framework into a direct vetting conversation with any bank marketing firm you are seriously considering.

- What does your discovery and brand strategy process look like before any creative or campaign work begins? A credible firm will describe a structured phase of four to eight weeks minimum, encompassing stakeholder interviews, competitive analysis, customer research, and documented brand positioning outputs before a single brief is written. Vague answers here signal a tactics-first operation.

- Can you walk me through a financial services engagement from brief to measurable business outcome? Press for specifics: timelines, milestones, attribution models, and the actual business metrics tracked. Deposit growth, new account acquisition rates, and conversion lift tied to named campaigns are the benchmarks that matter.

- How does your team handle regulatory compliance review, who owns that process, and at what stage? The right answer involves compliance integrated at inception, not appended at the end. Ask whether they use documented approval workflows and whether your legal team retains final sign-off authority.

- How do you maintain brand coherence across digital, social, content, and experiential channels for a single client? Look for centralized asset management, enforced brand guidelines, and cross-channel planning sessions that keep messaging unified without sacrificing channel-specific nuance.

- What is your philosophy when a client’s leadership wants to pursue a campaign direction that conflicts with the brand positioning you established together? The strongest partners push back with evidence, propose data-backed alternatives, and protect long-term brand integrity over short-term accommodation. An agency that simply agrees is not a strategic partner.

The Right Bank Marketing Firm Is a Brand Partner, Not a Vendor

The bank marketing firm that earns long-term trust starts with belief, not budget allocation. Every criterion explored in this guide points toward the same conclusion: tactical performance without strategic conviction produces diminishing returns, particularly as digital channels consume 65 to 70 percent of bank marketing budgets in 2026 and brand incoherence across those touchpoints becomes increasingly costly to reverse. Fragmenting your spend across disconnected campaigns without a unifying brand belief system does not scale. It erodes differentiation at precisely the moment competitive pressure from fintechs and neobanks demands clarity.

Evaluate every prospective partner against all seven criteria before narrowing to a shortlist. A firm that excels at performance metrics but cannot articulate what your institution stands for will optimize your campaigns into irrelevance over time.

Starfish brings more than 20 years of financial services branding experience, integrated capabilities spanning strategy through activation, and a Brand Creed framework engineered to sustain conviction across every touchpoint. Brand is treated as an operating system, not a campaign, ensuring alignment across strategy, messaging, identity, and customer experience.

The right partner does not just execute. It protects your brand’s soul. Contact Starfish to explore how a brand-first approach to bank marketing translates into measurable, lasting business impact for your institution.